There has been a significant growth in the numbers, and the overall cost, of the R&D tax Credits claims being made since about 2014.

R&D Tax Credits Stats -September-2021

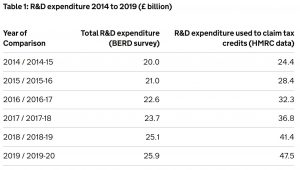

A disturbing chart in HMRC’s latest report (above) shows that the gap between HMRC data and ONS’s Business Enterprise Research and Development Survey (BERD) increased to over £20bn in 2019-20.

Whilst the two sets of figures are not directly comparable, the known differences (e.g. overseas expenditure is not included in BERD data) only partially explain the differences.

Concerns over the potential level of ‘false’ claims and a lack of resource to vet them, has led HMRC to plan for significant and urgent improvements to their compliance regime – some of which have already been implemented.

One step was to recruit an additional 100 compliance staff to work exclusively on examining R&D claims. These staff are now coming on stream. In addition various research efforts, including an increased level of random enquiry selections, were commenced to try to establish the scale of error and avoidance in R&D Tax Credit claims.

The Treasury also launched a consultation covering compliance issues on the R&D regime, which has already announced interim conclusion, and further consultation is taking place on new compliance measures to be introduced from April 2023.

Amongst the measures already announced are

- Further increases in the compliance staff resource

- A requirement that subcontracting and agency labour work for R&D be carried out in the UK in order to be eligible

- All claims will need to be made digitally and contain a lot more detail – for example on what expenditure the claim covers, the field of science or technology covered, the nature of the technology advances sought, and the technological uncertainties that needed to be overcome.

- Each claim will need to be endorsed as satisfactory by a named senior officer of the company

- Companies will need to alert HMRC to R&D relief claims in advance

- Companies will need to include details of any agent that has advised the company on compiling the claim.

Taken together, the compliance changes, and the hardening of the HMRC approach to claims represent a significant change in how HMRC will be approaching R&D tax Credits claims.

It seems particularly desirable now to avoid the risk of their intervention on future claims. For that reason it would be sensible to ensure that claims are presented in a way that covers, and deals with, any uncertainties so there may still be a good chance of HMRC accepting them without enquiry.

HMRC requirements for a satisfactory claim

Although there is no legal obligation to do more than enter an amount of the R&D Tax Credits claim in the tax return, HMRC will risk assess the claim, and without further information are likely to give it a high risk loading, making an enquiry more likely.

In addition, if an enquiry starts and then finds that amounts have clearly been wrongly claimed, HMRC could reopen earlier years and re-examine them, unless sufficient information was given at the time of submission so as to mean that HMRC have already had the opportunity to raise any issues (and hence they would be foreclosed from reopening the earlier years).

Both these factors make it desirable to produce a properly structured and presented claim.

HMRC have indicated what they want to see:

- A claim constructed in accordance with the definition of R&D contained in the BEIS guidelines, and the legislative requirements in CTA 2009. A well presented claim should make reference to these and demonstrate familiarity with them

- A claim that identifies specific R&D projects, in accordance with the Guidelines, detailing their advances and uncertainties in their respective fields of technology ( as identified by a Competent Professional in those fields). The advances should be benchmarked against the current technology state of play in the technology field, and, for the uncertainties, it should be explained why there were not already solutions within the knowledge base of a competent technology professional (or readily deducible from that knowledge base).

- Costings for each project, constructed by reference to the allowable categories of expenditure permitted by legislation

- Narratives that deal with each year of claim as separate claim periods, detailing the time lines for the projects and the work and challenges in each year.

- Information as to where the boundaries of the R&D projects have been set, and how the specific eligible costs of the R&D project have been identified ( as contrasted with the wider commercial project costs, or non-qualifying categories of expenditure)

- Information as to where any estimates have been needed and if so who has made them and on what factual, or business record, basis

A claim prepared by a reputable advisor should take account of all these aspects.