This is the second article in my three-part R&D Tax Credit Insider series on how the UK’s world-leading R&D incentive was brought to the brink by hype, political complacency and industry inaction.

Part two: The “£84 billion pot of unclaimed R&D Tax Credits”

The UK’s flagship R&D Tax Credit regime was once regarded by policymakers and international bodies as a model for supporting innovation, particularly for SMEs, but from 2013 it began to expand at a rapid and unsustainable pace.

In 2012-13, just 15,930 claims were made under the scheme. By 2021-22, the number had jumped to 90,315, a near six-fold increase in just nine years.

This explosive growth was not matched by an equivalent rise in HMRC enforcement of standards, resulting in a system that became increasingly vulnerable to abuse.

Incremental enhancements to the scheme’s generosity across multiple Budgets helped spark a deluge of questionable claims.

By the time serious concerns were raised regarding poor economic returns and rising fraud and error, the scheme was already in freefall.

A quiet consensus seemed to develop where advisors, accountants and claimants all exploited a regime that had steadily unravelled under HMRC’s watch.

The result was a tax relief that became synonymous with widespread misuse.

How was this allowed to happen?

Over time, HMRC’s grip on the R&D regime had loosened. Structural reforms, staffing cuts and an early culture of “pay now, check later” left the system exposed.

Without the technical expertise to assess claims properly, and under pressure to process payments quickly, HMRC’s oversight deteriorated.

Meanwhile, advisors and accountants moved swiftly to exploit the gap. Many claims became inflated, poorly evidenced and increasingly disconnected from genuine R&D activity.

This laid the groundwork for a flood of misleading messaging and overpromising from marketing-led advisory firms.

Two million SMEs “owed money”

A 2018 PR exercise, widely circulated at the time, came to symbolise many of the scheme’s emerging problems.

This was a research study undertaken on behalf of an R&D advisory firm, Catax, which claimed that vast amounts of SME R&D tax relief were going unclaimed.

The Catax survey alleged that companies were missing out on an £84 billion “SME war chest” of unclaimed R&D Tax Credits and that nearly 2 million SMEs were “owed money”.

Despite being based on highly speculative assumptions, the supposed £84 billion “pot of unclaimed R&D Tax Credits” took on a life of its own. It was cited in numerous articles which were eagerly consumed by a new generation of R&D advisory firms which saw a vast untapped market of up to 2 million companies that were eligible to claim R&D Tax Credits but weren’t currently doing so.

Even respected outlets such as Tax Journal seemed to accept the estimates at face value, confidently stating:

“Research carried out by tax relief specialist Catax suggests around £84bn in R&D tax relief available to SMEs remains unclaimed.”

Catax was quoted by Tax Journal as stating that valid R&D claims could be made for “even a new, innovative dish at a restaurant”.

The survey was also highlighted in this article from the Daily Express:

“The tax specialist’s [Catax] research showed that of the 3.5 million British small to medium sized enterprises (SMEs) actively trading, around 57 per cent or 1.9 million are eligible for R&D relief.

“However, it found only 1 per cent of those have actually claimed their tax credits.

“Catax says that as the tax credits are worth on average £43,000 to those that receive them, it calculates that if all the SMEs eligible claimed, it would cost the Government £84.2 billion”

These examples are just some of the outlets that repeated the startling claims derived from the Catax survey.

The tip of the iceberg?

The findings of this widely disseminated survey remained largely unchallenged until 2022 when certain details were passed to Lord Leigh of Hurley who was presiding over a House of Lords committee investigating the R&D Tax Credit regime.

Lord Leigh questioned a Catax representative about the survey during a House of Lords committee session and, having received no satisfactory answers, requested that Catax write a letter to the committee to explain the basis on which they had concluded that 2 million SMEs should be making R&D claims.

In its written response to Lord Leigh, Catax stated that:

“The UK was a very different place then [2018]. Awareness of the [R&D] scheme was believed to still be very low, despite R&D Tax Credits having been introduced in the year 2000. The intention of this exercise was to raise awareness and encourage companies to contact Catax to discover whether they could be entitled to tax relief”.

“Only 8% of the 5,400 potential new claimants we talk to each year go on to make a claim with Catax as we decide the rest do not qualify.”

This statement indicates that Catax rejected nearly 5,000 companies annually that approached them who were actively exploring the possibility of making an R&D claim.

It can be assumed that a majority of these companies were likely to have had their interest piqued by the widely publicised £84 billion figure, suggesting they were missing out on valuable relief.

It is entirely plausible that many of these businesses, despite being turned away by Catax, went on to approach less scrupulous R&D firms that were willing to work with almost any company.

While the campaign may have intended to raise awareness of R&D Tax Credits, it may also have inadvertently fuelled a surge in interest from businesses that ultimately did not qualify, with many of them having been led to believe, based on research apparently endorsed by the Institute of Chartered Accountants in England and Wales (ICAEW), that they could be among the nearly two million SMEs supposedly eligible for the relief.

The admission by Catax that it rejected 5,000 hopeful companies annually could indicate that many more companies may have progressed, unknown by Catax, towards making claims.

But what if the 5,000 companies disqualified by Catax were just the tip of the iceberg? The fact that Catax alone turned away 5,000 potential claimants per year suggests there may have been a much larger pool of interested businesses who, undeterred, went on to pursue claims elsewhere and possibly without undergoing the same level of scrutiny.

Just because all the instances where the Catax survey was publicised specifically mentioned Catax doesn’t necessarily mean that the companies considering an R&D claim would have gone on to approach Catax for advice.

Some would have spoken to their accountant. Many of those accountants would also have read that a body as authoritative as the ICAEW was suggesting that 57% of all the UK’s SMEs should be making R&D claims.

We will never know the full consequences of the Catax survey, but its impact was undeniably significant and we can plot the growth that took place in the number of R&D claims filed after the survey was released.

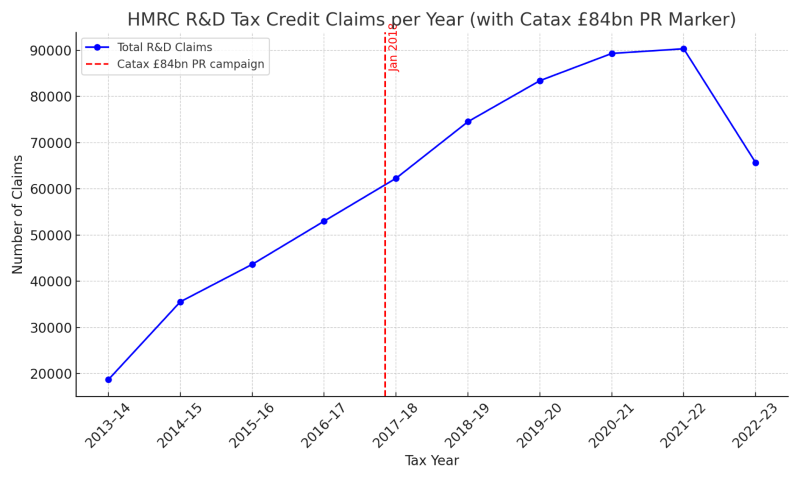

R&D Tax Credits for SMEs have now been around for 25 years; however, for the first 14 years of operation, the annual number of claims never exceeded 20,000.

From 2013-14, the number of R&D claims filed by SMEs began to grow rapidly. The graph (below) shows that by 2016-17 the total number of claims filed annually had increased to just over 50,000.

Whilst it’s impossible to prove a direct correlation between the Catax “£84 billion” campaign and the subsequent sharp rise in R&D claims from just over 50,000 to 90,000, it undoubtedly helped create the conditions that the wider R&D advisory industry rushed to exploit.

From “gold rush” to reckoning

The high-profile Catax PR exercise is still remembered across the R&D advisory industry for its lasting impact.

Despite being unsupported by HMRC data, both of the headline statistics (ie the supposed £84 billion in unclaimed R&D Tax Credits and the idea that nearly 2 million SMEs should be making claims) became the most widely circulated figures in the industry.

It contributed to a perception among some aspiring R&D advisors, accountants and SMEs that R&D Tax Credits were an untapped goldmine waiting to be “unlocked”.

For instance, is it a coincidence that three of the most controversial (but now defunct) R&D Tax Credit advisors of recent years were set up in immediate aftermath of the 2018 survey?

ZLX Ltd – incorporated 4 March 2019

Green Jellyfish (GJ2020 Ltd) – incorporated 1 July 2019

RDI Solutions Ltd – incorporated 21 December 2019

At the time, few in the industry publicly challenged the claims, perhaps because the narrative aligned with their own commercial interests.

One who did was Mark Evans who raised the matter with HMRC’s technical lead on R&D Tax Credits, Philip Hamblin, in February 2018.

Mark recalled that:

“[Hamblin] already knew all about the [Catax] issue. Obviously I had not been the only one upset by the Catax article. He said that it was being dealt with and he made it completely clear he was less than impressed with Catax. He later wrote to me saying “I await an explanation of the figures from the agent with interest”.

It is not known whether HMRC received a response from Catax or if any action was taken.

But from most of the R&D advisory and accounting industries there was silence.

The uncomfortable truth is that most advisors sat on their hands while the problems festered for at least 3 more years.

A culture developed in which the financial rewards from maintaining the status quo were simply too lucrative.

Even when R&D advisors saw others behaving recklessly or submitting implausible claims, few were willing to speak out. When anyone did raise concerns, they were often met with responses such as “don’t badmouth competitors”.

In hindsight, this mass-delusion is highly embarrassing for the R&D advisory industry. It was a period when many R&D Tax Credit advisors were engaged in a vigorous land-grab to secure as many clients as possible with a view to maximising business valuations before a trade sale.

The R&D advisory sector could and should have done more. Individually, many firms were concerned that things were getting out of hand, but collectively, nearly everyone was culpable by sharing in the profits from the rapid growth of R&D claim numbers.

The increased awareness of R&D Tax Credits from the Catax survey made marketing the scheme easier for many firms and they were only too happy to share in the spoils.

Most however knew deep down that the R&D scheme had to change.

One experienced R&D Tax Credit specialist I spoke to described the survey as “thoroughly irresponsible” and said “it should have been a wake-up call, not just for HMRC but to the entire R&D claims industry as an indication that the growth in claim numbers was becoming increasingly unsustainable”.

Even though we are now in a completely different world to where we were in 2018, the impact of the infamous Catax survey endures.

As recently as February 2025, unsubstantiated research undertaken by Wellers Accountants was reported to show that “UK SMEs are estimated to be missing out on a staggering £47 billion in potential tax savings”.

Whilst it may seem incredible to see history repeat itself, the fact that this new “research” was immediately and widely ridiculed highlights how far the industry has come in cleaning up its act in recent years.

Coming soon…. look out for part 3 of my “rise and fall of the UK’s R&D Tax Credit scheme series”

Article written by Rufus Meakin

Rufus Meakin works with tech companies to help ensure their R&D Tax Credit claims are accurate and defendable.

If you would like to discuss any aspect of your R&D Tax Credit claim, then please feel free to book an exploratory call here: https://calendly.com/rufusmeakin-uk/r-d-tax-credits-exploratory-call